Synopsis of the week

- The latest US reporting season kicked off with US Banks Citigroup and JPMorgan posting better than expected figures and an increase to their dividends.

- It appears US President Donald Trump can’t help himself from starting fights with everyone and every organisation he comes across, a list that now includes both the UK Prime Minister and NATO.

- Ahead of new trade tariffs being imposed on Chinese goods, the trade balance with the US has widened to US$29 Bn in June from US$22 in May.

Press coverage

On Wednesday evening, Alastair McCaig, our Head of Investment Management joined Bloomberg anchor Charlie Pellet and Richard Jones, FX & Rates Strategist. In this week’s show, they discussed the latest developments in Brexit policy from the Conservative government, the markets and how NATO’s meeting in Brussels was developing following President Trump’s comments.

Click here to listen to the interview on Bloomberg

US equity markets have again led the way for others to follow as they rounded off a second positive week. In Europe, the French CAC, German DAX and UK FTSE all managed to replicate this but in a considerably less convincing manner. The major US equity indices, the Dow, NASDAQ & S&P 500 are all up on the year and are now getting close to hitting the highs seen in January. Asia remains underwater as worries surrounding the US / China trade war continue to weigh on the region.

We have stated on numerous occasions this year, that we remain invested in the markets even though geopolitical events have seen volatility increase and investor confidence dented. These next few weeks, where we will see the US reporting season start again, are an important test as we wait to see if the fundamental data continues to warrant current equity share prices. When looking at US equity prices and the moves we have seen, it is worth remembering that current Price Earning multiples are at 17 times and the long-term average is 16.7 times. Using this as a barometer, share prices are not as overcooked as investors had previously assessed.

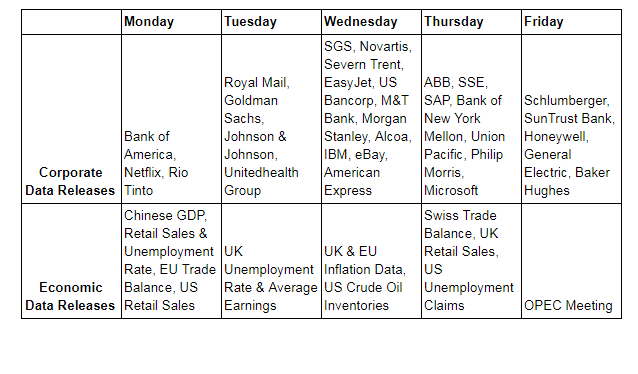

The start of the reporting season will be dominated by the US Banking sector. The first few days have seen JP Morgan, Citigroup and Bank of America all beat earnings expectations, increase their dividend sizes and either confirm or announce stock buyback programmes. This certainly sets an early positive precedent for the remainder of the US earnings season.

US President Donald Trump has a long list of global leaders and institutions that he has now met face to face and to a greater or lesser degree started an argument with. Last week, it was the turn of UK Prime Minister Theresa May and NATO (not to mention the lack of chivalry shown when meeting the Queen). This week, he will be meeting with Russian President Vladimir Putin, considering the investigation into the US election results and the suspicion that Russia interfered, this should provide plenty of column inches for the press to write about.