Synopsis of the week

- Theresa May’s speech at the Conservative party conference casts doubts on the UK’s ability to maintain passporting rights with the EU sending Sterling spiralling lower.

- The collapse of the UK Pound against the US Dollar has boosted the FTSE as 80% of the companies in the index see their income derived from US Dollars.

- News that the European Central Bank were analysing how to start tapering their €80 Billion monthly Quantitative easing scheme gave European equities a mid-week wobble.

- Friday’s Non-farm payrolls miss the mark but not by enough to shift market expectations of a Fed rate rise in December.

The Week Ahead

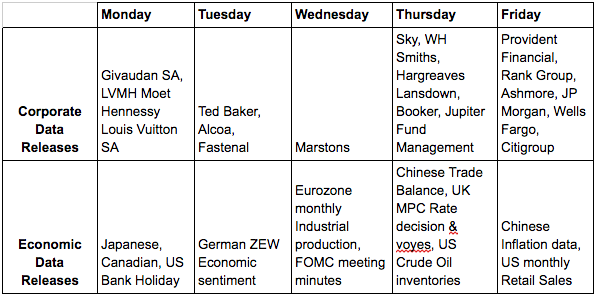

Economic Data

What a week we have just had. Political comments from both UK PM Theresa May at her Conservative party conference and French PM Francois Hollande, have driven GBPUSD down creating new 30 year lows. In little over three months since the Brexit vote the Pound has dropped by 25.46% against the US Dollar, hitting these levels in the “flash crash” during Thursday’s overnight Asian trading. The crux of this matter revolves around the EU’s demands that business passporting rights will only be maintained if the UK keeps to the EU’s rules on the free movement of workers. Considering tightening border controls was one of the key issues during the Brexit debate, this point is unlikely to be resolved any time soon.

Friday’s Non-Farm payroll figures came in short of the markets expectations but not by a large enough margin that they have changed expectations of a December rate rise. Fed chair Janet Yellen has made it clear the FOMC would like to raise interest rates but that it was “data dependant” if it were not for the US elections being only six days from the November meeting we could well have seen the board vote for action sooner in the year.

Corporate releases

Once again Alcoa will kick start the latest US reporting season on Tuesday afternoon. The aluminium manufacturer is always an interesting bellwether to how the US economy is behaving.

We’re not expecting many UK company announcements this week. However with the sizeable move we’ve seen in the strength of the Pound over the last week, we would not be too surprised to see companies make impromptu comments. Considering 80% of the FTSE 100 derive their profits in US Dollars it’s no surprise to see this index flying. The same can’t be said for other UK quoted companies outside the top 100 who will find their costs rising for any imports they require.

On Friday we’ll see the first tranche of US banks post their quarterly figures with Citigroup, Wells Fargo and JP Morgan all announcing figures. If anything this will highlight how much further down the road of recovery US banks are in comparison to the likes of Deutsche Bank and Commerzbank in Europe. Philip Hammond the UK’s Chancellor confirmed to the markets on Friday that plans to sell off the government’s holdings in both Royal Bank of Scotland and Lloyds have been shelved. This highlights clearly the divide in risk appetite to banks on either side of the Atlantic.

Image by PublicDomainPictures from Pixabay